This case study demonstrates how a Small Business Restructure (SBR) — combined with carefully considered refinancing, enabled our client to resolve a large tax debt, avoid personal tax exposure, and retain their ongoing business. While we typically advise against using personal assets like the family home to repay business debt, this scenario highlights an important exception: where limited strategic refinancing supports a well-planned restructure, protects personal equity, can deliver lasting financial stability. It also reinforces a key message for advisors supporting clients in distress: early intervention and specialist guidance really do matter.

—

Our client, a subcontractor in the construction sector, operated through a company that became insolvent after the collapse of a major builder. The fallout left them $600,000 out of pocket, with a matching $600,000 debt owed to the ATO and no means to pay. They faced immediate potential risks, including:

- The ATO disclosing the debt to credit reporting agencies

- Director Penalty Notices, making the debt personal

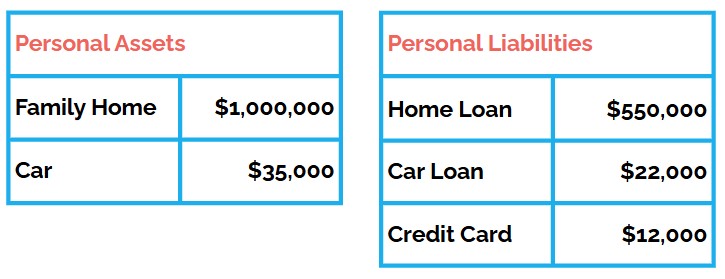

The client’s broker suggested refinancing the client’s family home to pay the ATO debt. Here’s a snapshot of our client’s personal finances:

Available Equity at 80% LVR: $244,000

Problem: This equity is not enough to pay the company’s $600K ATO debt.

This is where many clients can feel overwhelmed. With partial equity available and mounting pressure, they may rush into refinancing without understanding their options. This is the point where you as an advisor can make all the difference — by pausing their panic and connecting your clients to the early help of a specialist — before decisions with lasting financial consequences are made.

The Options that de Jonge Read Explored

Upon review, our team determined that an SBR was a right fit for this client – but we always assess other available options, for example:

1. Borrow what’s available ($244K) and try to negotiate the rest with the ATO

This approach offered no certainty, still exposed the director personally and there could still be risks of enforcement action on our client – hence this option was not recommended.

2. Enter a Small Business Restructure (SBR)

An SBR is a formal insolvency process, available to eligible small companies, where debts are compromised (often significantly), and the business continues under the same management. This option offered clarity, control, and a sustainable outcome for our client.

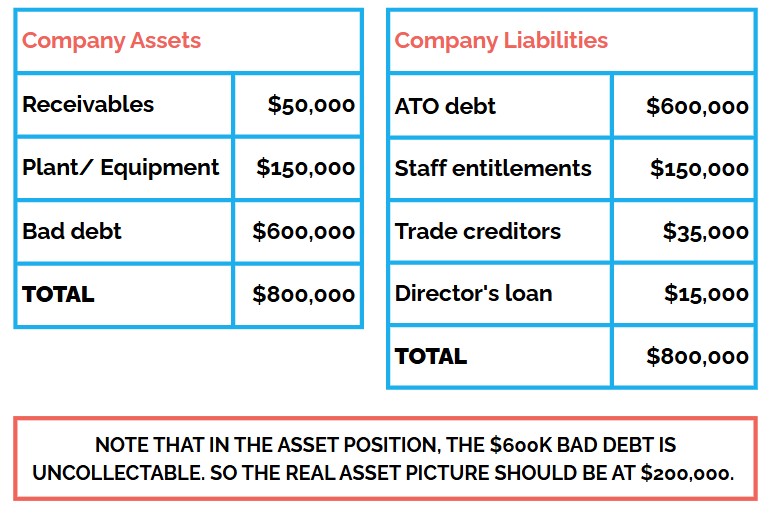

Snapshot BEFORE an SBR

The net position of the company is: -$600,000. An SBR can provide a structured, viable path forward – especially when paired with strategic funding.

The Outcome AFTER an SBR + Limited Refinancing

Using an SBR, we assisted our client to successfully settle their $800,000 debt for $160,000 i.e. 20 cents in the dollar, an outcome in line with de Jonge Read’s current average SBR settlement rate.

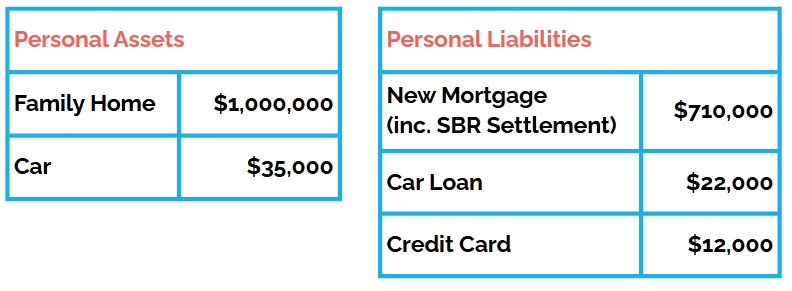

Our client’s personal snapshot AFTER an SBR

Net Personal Equity: $291,000 (up from $244,000)

Key outcomes achieved

- Business survived

- Director avoided personal liability

- No credit defaults

- The ATO and creditors received a reasonable return

- Staff entitlements were addressed

By design, once the SBR is successfully completed, the company is relieved of its admissible debts and can focus on growth and profitability. This approach when paired with targeted funding offered our client breathing room, debt relief and a clear path forward – all while preserving personal and business reputation.

Why We Supported Limited Refinancing in This Case

At de Jonge Read, we rarely recommend using personal assets like the family home to fund a business debt. However, in this instance, the refinance was strategic not reactive – a means to finalise financial distress, not extend it.

By borrowing $160,000 (in addition to the existing mortgage), not $600K, enabled our client to:

- Complete the SBR

- Retain their business

- Avoid personal liability

- Maintain a clean credit record

- Improve personal net equity (from $244K to $291K)

Refinancing alone won’t fix insolvency. But when used to support formal, affordable restructure, it becomes part of the viable solution.

—

At de Jonge Read, we:

- Assess SBR eligibility at no cost

- Manage the full restructure process – from liaising with creditors to formal practitioner appointment

- Coordinate and secure appropriate fundings with brokers and lenders

- Protect director’s interests throughout the process

We bring financial, legal, and practical expertise together to help clients achieve the best possible outcome — without disrupting business relationships or walking away from the business they’ve built.

As financial advisers, brokers, and accountants supporting clients in financial distress, you’re often first to hear when a business is struggling. When debts escalate, or ATO pressure builds, it’s important to recognise when specialist guidance is needed. Timely advice can make all the difference — preserving a client’s business, protecting personal assets, and achieving a stable way forward. Here’s how you can help:

- If your client is considering refinancing to repay an ATO debt – pause and check if an SBR might be a better fit

- If your client is unsure how to move forward – book ano-cost, no-obligation consultation with us at de Jonge Read

- If creditors are circling – engage us early, don’t wait until the wolves are at the door

An SBR can be a powerful, ATO-supported solution that helps businesses stay alive and relieves directors from the weight of unsecured debt. When paired with the right funding structure — such as limited, strategic refinancing, it can deliver outcomes that are practical, sustainable and achievable.

If you’re unsure whether a client qualifies, or how to structure the best path forward, reach out. At de Jonge Read, we manage the entire restructure process — from eligibility assessments to preparing proposals and working with creditors and lenders.

We make it simple, we keep it clear, and we’re here to help you support your clients in achieving the best possible result.

Should you have clients or associates that you know are struggling with financial issues or need assistance in reviewing their business affairs in preparation for what’s around the corner, our team of Strategists would be pleased to discuss options that are available on how to best design and implement insolvency strategies. Contact us now on p. 1300 765 080 | ua.mo1743672860c.arj1743672860d@ofn1743672860i1743672860

Did you know?

Phoenixing is another name of business restructure. Read more about business restructures and when this can be an option for you.